SUPPLEMENTARY

BUSINESS PAPER

(Item 18)

General Meeting

Wednesday 14 July 2021

at 6:30PM

SUPPLEMENTARY

BUSINESS PAPER

(Item 18)

General Meeting

Wednesday 14 July 2021

at 6:30PM

Hornsby Shire Council Table of Contents

Page 0

SUPPLEMENTARY ITEMS

Item 18 PC14/21 Development Contributions Reforms................................. 1

Director's Report No. PC14/21

Planning and Compliance Division

Date of Meeting: 14/07/2021

18 DEVELOPMENT CONTRIBUTIONS REFORMS

EXECUTIVE SUMMARY

· To progress reforms to the infrastructure contributions system, the Government introduced the Environmental Planning and Assessment Amendment (Infrastructure Contributions) Bill 2021 to Parliament on 22 June 2021. The Bill has been referred to an Upper House Committee for further inquiry.

· Although some aspect of the changes proposed may be positive, others have potential for significant adverse financial impact on Council. It is evident that further consultation is required with councils to ensure changes are positive for the community.

· It is recommended that Council make a submission to the parliamentary inquiry into the Environmental Planning and Assessment Amendment (Infrastructure Contributions) Bill 2021 in accordance with the contents of this report.

|

THAT: 1. Council make a submission to the parliamentary inquiry into the Environmental Planning and Assessment Amendment (Infrastructure Contributions) Bill 2021 in accordance with the contents of Director’s Report No. PC14/21 and raising matters including the following: a. The reforms appear to be inconsistent with Government objectives for jobs creation by reducing the capacity for Council to fund the delivery of community infrastructure with associated construction jobs. b. The issue of rate reform should be uncoupled from the review of development contributions to ensure the cost of providing new facilities to meet the needs of a growing population is not shifted to the existing community. c. Implementation of the recommendations will potentially have far reaching financial implications for councils and communities requiring further detailed modelling by the State Government at the individual council level. d. Clarification is required concerning the definition of “development contingent infrastructure” and what infrastructure will be retained on the Essential Works List. e. Recognising that Section 7.12 levies for alterations and additions to residential dwellings in infill areas is an appropriate method of funding the provision of community infrastructure. f. The point at which payment of developer contributions is made should be maintained at the submission of construction certificates. 2. The General Manager be delegated to carry out further actions to support raising the matter with the State Government during the caretaker period for the upcoming local government elections. 3. A copy of Council’s submission be forwarded to local State Members of Parliament. |

PURPOSE

The purpose of this Report is to seek Council endorsement to make a submission to the Upper House Committee Inquiry into the Environmental Planning and Assessment Amendment (Infrastructure Contributions) Bill 2021

BACKGROUND

Contributions for local infrastructure, also known as developer contributions, are charged by councils when new development occurs. They are used to provide infrastructure to support development, including open space, parks, community facilities, local roads, footpaths, stormwater drainage and traffic management.

There are two forms of local infrastructure contributions. Section 7.11 contributions are charged where there is a demonstrated link between the development and the infrastructure to be funded. Councils prepare contributions plans which specify what infrastructure will be provided and approximately how much it will cost. Section 7.12 levies are an alternative to s7.11 contributions and are charged as a percentage of the estimated cost of the development. For these types of levies, a direct nexus between the development and identified works is not required.

Council contribution plans are generally limited to the costs of providing infrastructure needed to cater for a growing population. The ongoing costs of managing and maintaining infrastructure are not included in these plans and are funded through rates and other income streams. This is increasingly becoming a significant financial challenge for councils.

The development contribution system in NSW is overly complex and an administrative burden for councils. Therefore, when the State Government announced its intention to review the development contributions system, Council indicated its support for a review aimed at reducing complexity and improving the transparency of the current system.

Productivity Commission Review

In 2020, the NSW Productivity Commission undertook a holistic review of the Local Contributions System in NSW. The final report on the review was released in November 2020, with a package of reforms which impact on local councils’ capacity to fund local infrastructure and collect contributions.

The Commission noted that NSW will face a constrained budgetary position as the recovery from the COVID-19 pandemic progresses, asset recycling winds down, and pressures from a growing and ageing population increase. All levels of government will need to reconcile the need for fiscal repair with increasing demands for infrastructure.

In March 2021, the NSW Government confirmed it had accepted all 29 recommendations of the final report. A framework is expected to be established by 1 July 2022 and apply to new developer contributions plans and draft plans that have not yet been publicly exhibited.

The State Government is also planning to reform the rates system following a 2016 review by IPART. As part of the reform process, the Government engaged the Centre for International Economics (CIE) to model the financial impacts of the Productivity Commission’s proposed reform package (December 2020), including the revenue projections from:

· reform of the local government rate peg to enable rates revenue to grow in line with population. Currently, the rate peg does not allow for any growth in line with population growth in each council area; and

· adjustments to local infrastructure contributions to restrict the use of planning agreements, increase the threshold for some S7.12 levies and allow S7.11 contributions for development-contingent costs only.

In general, CIE’s results showed that under the combined set of reforms, councils will gain increased revenue from rates, but decreased revenue from infrastructure contributions, compared to what would be expected with current policy settings. However, these findings are disputed as outlined below in this report. Further, it is submitted that the use of rates to pay for infrastructure and facilities required by new development is fundamentally flawed and in direct conflict with the “user pays principle” under which contributions have historically been levied and would instead shift this cost burden to existing residents.

Infrastructure Contributions Bill

To progress the reforms to the infrastructure contributions system, the Government introduced the Environmental Planning and Assessment Amendment (Infrastructure Contributions) Bill 2021 to Parliament on 22 June 2021. However, due to extensive concerns raised about the impacts of the Bill, it has been separated from the other State budget bills and has been referred to an Upper House Committee for further inquiry.

The Inquiry will gather evidence on the implications of each proposed amendment and determine the appropriateness of the proposed amendments towards enhancing the contributions system. Submissions to the Inquiry closed on 11 July 2021 and the Inquiry is required to report by 10 August 2021. An extension of time was requested and has been granted until 15 July 2021 to enable Council to consider its position on the matter and make a submission.

DISCUSSION

This report outlines the findings of a review of the contribution reforms by the Northern Sydney Region Organisation of Councils and outlines the implications of the proposed changes for Hornsby Shire.

NSROC Review

To assist evaluation of the proposed changes to the development contribution system, planning consultants, GLN Planning, were engaged by the Northern Sydney Region Organisation of Councils (NSROC) to undertake a holistic review of the reform impacts on member councils, including rate peg reform impacts.

It is essential that councils are not left worse off by the NSW Government’s infrastructure contributions reform agenda and the Government’s modelling indicates that the reforms will benefit councils. However, the consultant’s modelling of what is known indicates a contrasting view. The consultant’s modelling shows significantly reduced contributions income for most metropolitan councils with declines likely for both s7.11 contributions and s7.12 fixed-rate levy projected income levels. The specific implications of the changes for Hornsby Shire are discussed below.

Section 7.11 Development Contributions Plan

The Hornsby Section 7.11 Development Contributions Plan 2020 - 2030 came into force on 3 August 2020 and applies to all new residential and commercial development including subdivision, new dwellings, seniors housing (excluding residential care facilities), retail premises, business and office premises.

The Plan is largely based on providing additional services to cater for forecast growth within areas rezoned for higher density residential development as part of Council’s Housing Strategy to meet State Government obligations for housing provision. To cater for anticipated growth, the Plan includes an extensive works schedule of road, local open space, recreational and community facilities projects with total costs over $340 million with $157 million of those costs to be levied from development contributions. Of note, the works program includes significant funding for the delivery of the following projects:

· Hornsby Park - $28 million

· Westleigh Park embellishment - $16 million

· Asquith Town Centre Public Domain Improvements - $13 million

· Hornsby Central library - $15 million

· Hornsby Community Centre - $13 million

· Pennant Hills library - $12 million

The reforms raise significant risks for projected S 7.11 contribution income as a result of the proposal that the extent of the works schedule be limited to “development-contingent” works. There is currently little clarity on what “development-contingent” works would be in an infill context.

The GLN Report notes that it could be assumed that development-enabling infrastructure such as transport and stormwater works will be considered “development-contingent” but that community and indoor recreation facilities probably would not. The provision of these facilities is generally not essential for development to proceed and they often provide benefits to the broader community. They are also infrastructure types that do not appear on the current essential works list used by IPART when assessing contributions plans.

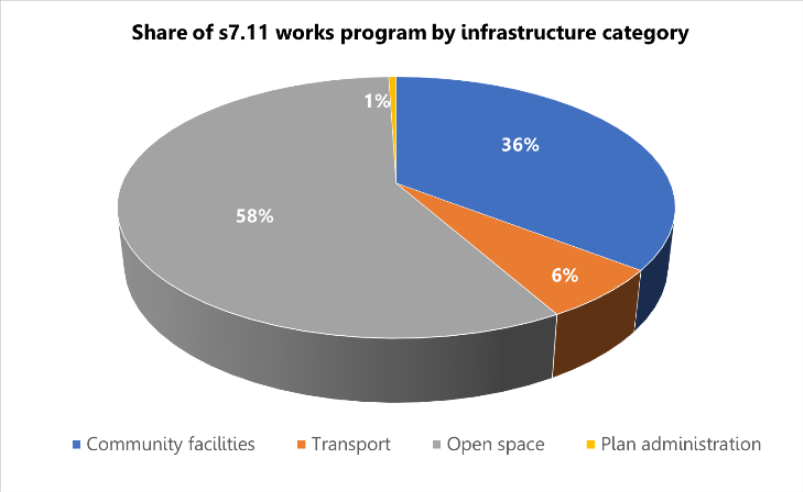

On average, community and indoor recreation facilities represent 36% of the Council’s works program costs where s7.11 contributions are levied (as shown in the graph below) and these costs could be excluded from s7.11 plans from 2024/25.

The GLN Report notes that the removal of the ability to levy contributions for community and indoor recreation facilities would result in a potential loss of income under Council’s s7.11 Contributions Plan in the order of $90 million over the next 17 years (being the period from the proposed commencement of the changes in 2024 to 2041). This figure is calculated as 36% of contributions from the projected 774 dwelling completions annually. The number of dwellings is based on average building approvals over the last 3 years.

Alternatively, Council’s income from S7.11 contributions over the last 5 years is indicated in the table below.

|

Year |

2016/17 |

2017/18 |

2018/19 |

2019/20 |

2020/21 |

Total |

|

Income |

$19,107,274 |

$11,698,875 |

$9,906,519 |

$4,605,527 |

$2,922,226 |

$48,240,421 |

Projecting the average income of $9.6 million received over the next 17 years and applying 36% for community and indoor recreation facilities would result in a potential reduction of income in the order of $59 million. Therefore, the loss of income under Council’s s7.11 Plan would potentially be $90 million to $59 million.

Such a significant reduction in anticipated contributions income would reduce Council’s capacity to deliver the extent of planned infrastructure to support population growth. One of the main issues raised by the Hornsby Community in community satisfaction surveys is resident concerns about the impacts of increased residential development and the need to augment community facilities to cater for growth. The estimated reduction in funds would severely restrict the provision of open space, public domain improvements and community facilities which are essential components of creating liveable, attractive and sustainable communities.

Section 7.12 Development Contributions Plan

The Hornsby Section 7.12 Plan 2019-2029 applies to additions and alterations to residential development, alterations to commercial development, industrial development, residential care facilities and any other development. The Pan includes a work schedule identifying $7.85 million in projects to be funded including street tree planting, playground shade devices, off leash dog facilities, solar panel installation at the Hornsby Aquatic Centre and Community Recycling Centre, Hornsby Library expansion, bushland reserve infrastructure, footpath and playground improvement.

In accordance with the Plan, contributions are not levied for development where the costs of work are less than $100,000. However, a 0.5% levy applies for development with a cost of $100,000 - $200,000 and 1% for all development over $200,000.

As indicated in the table below, Council has received almost $7.2 in levies under the Plan in the last 5 years.

|

Year |

2016/17 |

2017/18 |

2018/19 |

2019/20 |

2020/21 |

Total |

|

Income |

$1,304,445 |

$1,518,422 |

$1,735,319 |

$1,372,717 |

$1,252,163 |

$7,183,066 |

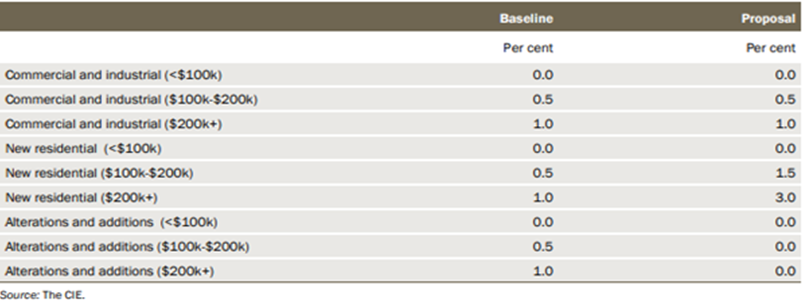

Most of the income received under the Plan is associated with the applications for alternations and additions to residential dwellings. The draft reforms include a proposal that contributions would only be payable for new dwellings or where new employment generating floor space (commercial or industrial is proposed) as outlined in the table below.

Applications for new dwellings are currently levied contributions under Council’s s7.11 Contributions Plan. Therefore, the proposal to increase the per centage for new residential (dwellings), although welcomed, would not benefit the operation of Council’s existing 7.12 Plan. Conversely, the proposal to exempt alterations and additions and instead only apply the levy to net additional floor area would have significant impact on income and associated delivery of new projects.

Most of the development in Hornsby Shire is for residential alterations additions which would no longer attract development contributions under the proposals. Based on ABS Building Approvals data, the GLN Report estimates that this change has the potential to cost Council in the order of $920,000 annually or $15.6 million over the next 17 years. However, based on income received over the last 5 years, this change may be more significant, with an estimated loss of $1.2 million annually or $20 million over the next 17 years.

Rate Pegging

In summary, the above changes have the potential to costs Council in the order of $106 million to $79 million in lost development contributions over a 17-year period.

The State Government proposes that the reduced funding from development contributions to councils is to be offset by the increase in rates revenue with the addition of the population growth factor.

However, the June 2021, Independent Pricing and Regulatory Tribunal (IPART) Review of the Rate Peg to include Population Growth states that councils are not adequately compensated for population growth under the current rating system, which disincentivises them from accepting development and population growth. It is recommended that each councils’ general income on a per capita basis should be maintained as its population grows.

The GLN report similarly notes that it does not follow, as suggested by the PC, that a council that receives extra rates income from the introduction of the population growth factor will apply that income towards meeting the capital cost of works and land acquisition for infrastructure that is generated by new development. It will more likely be spent on the marginal operational (rather than capital) costs incurred by the council in maintaining the asset base. This is both the existing asset base and the additional assets funded by infrastructure contributions and constructed or handed over to the council.

The GLN Report calculates an average population growth of 1% based on 744 dwellings and 1,596 residents per annum to 2041 and an increase of new workers of 265 for the same period. This population increase would provide in the order of $101 million in additional rates income over the next 17 years which would be marginal in terms of offsetting the loss in developments contributions income over the same period.

Rates have historically been collected by Council for service delivery and maintenance of assets and not for provision of new facilities to meet the demands of new development. Although rate reform is welcomed, the issues of rate pegging should be uncoupled from the issue of developer contributions which has a different purpose.

OTHER DRAFT LEGISLATIVE AMENDMENTS

It is apparent that through the proposed amendments to S7.11 and 7.12 plans, the State Government is focused on reducing development costs to support the construction industry to increase investment and job opportunities. However, this aim should be balanced against the potential loss of income to councils and delay in the provision of community infrastructure projects which have similar investment and job creation opportunities.

The current reforms would at best see cost shifting for provision of community infrastructure to the existing community through rate reforms. At worst, projects may be significantly delayed or not progressed at all. Accordingly, further financial modelling at the individual council level is required to demonstrate the financial benefits of the proposed reforms. Further, the issue of rate reform should be separated from the review of the development contributions legislation.

The following discussion provides specific comment on other components of the proposed legislative changes under the draft Bill.

Introduction of a Land Value Contribution Mechanism

A new framework to enable councils to require landowners in an identified precinct to contribute towards land required for public purposes would appear to have merit as increasingly, the acquisition of land is becoming unaffordable for many councils. However, more detail and clarity about how this proposal would operate is required to enable an informed position and response.

Council has also advocated that value capture through a planning agreement is an important tool to enable councils to deliver infrastructure that is required to meet the demands of future populations over and above a s7.11 or s7.12 plan, where the current Ministerial Thresholds limit the levying for such infrastructure. Accordingly, as part of the review process, value capture should continue to be recognised as an appropriate mechanism to use.

Pooling of Development Contributions

Proposed changes to enable councils to pool contributions without the need for a Ministerial Direction for contribution plans to allow it should be supported.

The Hornsby Section 7.11 Development Contributions Plan currently expressly authorises monetary contributions paid for different purposes to be pooled and applied (progressively or otherwise) for those purposes. The priorities for the expenditure of the levies are shown in the works schedule in the Plan. The pooling of funds is an appropriate practice to assist the timely and efficient delivery of projects identified in a contributions plan.

Deferred Payment of Contributions to Occupancy Certificate Stage

It is proposed that developer contributions would be payable at occupancy rather than before construction starts. This was originally announced as a COVID response by the Government but is now proposed as a permanent policy position. This amendment is inconsistent with the purpose of levying contributions to seek to ensure that community infrastructure is delivered in a timely manner in conjunction with development.

Councils would not receive the funds to provide community facilities until after development has occurred which is not sound planning practice. Further, this would also be inconsistent with the State Government’s objective for economic growth in the development sector due to the loss of jobs generated through the design, development, delivery and operation of these public facilities.

Alternatively, councils would be required to forward fund infrastructure delivery at a financial burden to the council and its existing rate payers. Council has limited capacity to forward fund major infrastructure projects while awaiting contribution payments from developers.

Experience has shown that ensuring follow up non-payment of contributions at the occupancy stage is a further administrative burden on councils. This is because Council does not always have control over the full or partial occupation of buildings (i.e. when a private certifier is used) and there is a significant risk that occupation occurs without contributions being paid. The burden then falls to Council to act against the private certifier and potentially occupants of the building or the body corporate which is a difficult process.

The current arrangements for payment of contributions at the constructions stage should be maintained to facilitate the timely delivery of infrastructure with development.

Adopt Regional Infrastructure Contributions

Previously analysis at both the NSROC and Hornsby Shire level indicates that major recreation and sporting facilities address regional demand beyond local government area boundaries. The Hornsby Park and Westleigh Masterplan projects are examples of the provision of such facilities which will provide open space and recreational opportunities for the North District and beyond. Development contributions will assist the delivery of these projects. However, the delivery of these projects is also reliant on significant grants at the State level. Therefore, levies across multiple LGAs that cannot be met through s7.11 development contributions are supported in concept.

However, any such levies should not come at the expense of local development contributions. These levies should also align with strategic planning priorities in district and local plans, in addition to producing tangible public benefits for the community. More detail and analysis are required concerning this proposal in terms of how it would relate to local contributions and delivery of services.

Use of Digitised tools to make Contributions Simpler and more Transparent

Improvements in reporting infrastructure contributions to make the system more user friendly, transparent and efficient are welcomed. However, the reforms encompass potential increased administrative and compliance burdens for local councils in the short to medium term, particularly related to the needs of the new centralised (digitised) contributions system, the amendments to plans and the integration of the plans within the Integrated and Performance Reporting Framework (IP&R) framework.

The proposed changes include a requirement that councils integrate their local infrastructure contributions systems into their IP&R Framework and review their infrastructure contributions plans by 1 July 2024, and every four years thereafter (or earlier if required), to align with their delivery program. Although supported in principle, further detail and consultation is required with councils to assist understand the resource implications of implementing any new framework.

BUDGET

There are no budgetary implications associated with this Report. Scoping of a digital tool as referenced above will be conducted with existing budget allocations.

POLICY

The proposed legislative changes to the development contributions system would have significant financial implications for Council as outlined in the report..

CONCLUSION

Council has advocated in support for reform of the development contribution system in NSW for many years with the aim of reducing complexity, improving transparency and equity and releasing the financial burden placed on councils to provide local infrastructure to support population growth. Although some aspect of the changes proposed by the State Government may be positive, others have potential for significant adverse financial impact on Council and its ability to provide community facilities for its residents. It is evident that further analysis and consultation is required with councils to ensure changes are positive for the community before implementation. Accordingly, it would be appropriate that Council make a submission to the parliamentary inquiry into the Environmental Planning and Assessment Amendment (Infrastructure Contributions) Bill 2021 in accordance with the contents of this report.

RESPONSIBLE OFFICER

The officer responsible for the preparation of this Report is the (Director, Planning and Compliance) – (James Farrington) - who can be contacted on 9847 6750

|

James Farrington Director - Planning and Compliance Planning and Compliance Division |

Steven Head General Manager Office of the General Manager |

There are no attachments for this report.

File Reference: F2010/00015-04