BUSINESS PAPER

WORKSHOP Meeting

Wednesday 23 November 2022

at 6:30pm

BUSINESS PAPER

WORKSHOP Meeting

Wednesday 23 November 2022

at 6:30pm

Hornsby Shire Council Table of Contents

Page 0

AGENDA AND SUMMARY OF RECOMMENDATIONS

Rescission Motions

Mayoral Minutes

ITEMS PASSED BY EXCEPTION / CALL FOR SPEAKERS ON AGENDA ITEMS

GENERAL BUSINESS

Office of the General Manager

Item 1 GM34/22 Adoption of a Draft Long Term Financial Plan for 2023/24 – 2032/33 and Progression of a Special Rate Variation Application for 2023/24....................................................... 1

Corporate Support Division

Nil

Community and Environment Division

Nil

Planning and Compliance Division

Nil

Infrastructure and Major Projects Division

Nil

PUBLIC FORUM – NON AGENDA ITEMS

Questions with Notice

Mayor's Notes

Notices of Motion

SUPPLEMENTARY AGENDA

MATTERS OF URGENCY

Hornsby Shire Council Agenda and Summary of Recommendations

Page 0

AGENDA AND SUMMARY OF RECOMMENDATIONS

PRESENT

NATIONAL ANTHEM

OPENING PRAYER/S

Acknowledgement of RELIGIOUS DIVERSITY

Statement by the Chairperson:

"We recognise our Shire's rich cultural and religious diversity and we acknowledge and pay respect to the beliefs of all members of our community, regardless of creed or faith."

Acknowledgement of Country

Statement by the Chairperson:

"Council recognises the Traditional Owners of the lands of Hornsby Shire, the Darug and GuriNgai peoples, and pays respect to their Ancestors and Elders past and present and to their Heritage. We acknowledge and uphold their intrinsic connections and continuing relationships to Country."

Video and AUDIO RECORDING OF COUNCIL MEETING

Statement by the Chairperson:

"I advise all present that tonight's meeting is being video streamed live via Council’s website and also audio recorded for the purposes of providing a record of public comment at the meeting, supporting the democratic process, broadening knowledge and participation in community affairs, and demonstrating Council’s commitment to openness and accountability. The audio and video recordings of the non-confidential parts of the meeting will be made available on Council’s website once the Minutes have been finalised. All speakers are requested to ensure their comments are relevant to the issue at hand and to refrain from making personal comments or criticisms. No other persons are permitted to record the Meeting, unless specifically authorised by Council to do so."

APOLOGIES / LEAVE OF ABSENCE

political donations disclosure

Statement by the Chairperson:

“In accordance with Section 10.4 of the Environmental Planning and Assessment Act 1979, any person or organisation who has made a relevant planning application or a submission in respect of a relevant planning application which is on tonight’s agenda, and who has made a reportable political donation or gift to a Councillor or employee of the Council, must make a Political Donations Disclosure Statement.

If a Councillor or employee has received a reportable political donation or gift from a person or organisation who has made a relevant planning application or a submission in respect of a relevant planning application which is on tonight’s agenda, they must declare a non-pecuniary conflict of interests to the meeting, disclose the nature of the interest and manage the conflict of interests in accordance with Council’s Code of Conduct.”

declarations of interest

Clause 4.16 and 4.17 of Council’s Code of Conduct for Councillors requires that a councillor or a member of a Council committee who has a pecuniary interest in a matter which is before the Council or committee and who is present at a meeting of the Council or committee at which the matter is being considered must disclose the nature of the interest to the meeting as soon as practicable. The disclosure is also to be submitted in writing (on the form titled “Declaration of Interest”).

4.16 A councillor who has a pecuniary interest in any matter with which the council is concerned, and who is present at a meeting of the council or committee at which the matter is being considered, must disclose the nature of the interest to the meeting as soon as practicable.

4.17 The councillor must not be present at, or in sight of, the meeting of the council or committee:

· at any time during which the matter is being considered or discussed by the council or committee, or

· at any time during which the council or committee is voting on any question in relation to the matter.

Clause 5.10 and 5.11 of Council’s Code of Conduct for Councillors requires that a councillor or a member of a Council committee who has a non pecuniary interest in a matter which is before the Council or committee and who is present at a meeting of the Council or committee at which the matter is being considered must disclose the nature of the interest to the meeting as soon as practicable. The disclosure is also to be submitted in writing (on the form titled “Declaration of Interest”).

5.10 Significant non-pecuniary conflict of interests must be managed in one of two ways:

· by not participating in consideration of, or decision making in relation to, the matter in which you have the significant non-pecuniary conflict of interest and the matter being allocated to another person for consideration or determination, or

· if the significant non-pecuniary conflict of interest arises in relation to a matter under consideration at a council or committee meeting, by managing the conflict of interest as if you had a pecuniary interest in the matter by complying with clauses 4.16 and 4.17.

5.11 If you determine that you have a non-pecuniary conflict of interest in a matter that is not significant and does not require further action, when disclosing the interest you must also explain in writing why you consider that the non-pecuniary conflict of interest is not significant and does not require further action in the circumstances.

Petitions

presentations

Rescission Motions

Mayoral Minutes

ITEMS PASSED BY EXCEPTION / CALL FOR SPEAKERS ON AGENDA ITEMS

Note:

Persons wishing to address Council on matters which are on the Agenda are permitted to speak, prior to the item being discussed, and their names will be recorded in the Minutes in respect of that particular item.

Persons wishing to address Council on non agenda matters, are permitted to speak after all items on the agenda in respect of which there is a speaker from the public have been finalised by Council. Their names will be recorded in the Minutes under the heading "Public Forum for Non Agenda Items".

GENERAL BUSINESS

1. Items for which there is a Public Forum Speaker

2. Public Forum for non agenda items

3. Balance of General Business items

Office of the General Manager

Page Number 1

Item 1 GM34/22 Adoption of a Draft Long Term Financial Plan for 2023/24 – 2032/33 and Progression of a Special Rate Variation Application for 2023/24

RECOMMENDATION

THAT:

1. The contents of General Manager’s Report No. GM34/22 and Morrison Low’s Community Engagement Outcomes Report, which provide details of the outcome of the public exhibition process conducted between 4 October 2022 and 8 November 2022 in respect of Council’s draft Long Term Financial Plan (LTFP) for 2023/24 to 2032/33 and Council’s intention to make application for a Special Rate Variation (SRV) for the 2023/24 financial year, be received and noted.

2. Council advise the Independent Pricing and Regulatory Tribunal (IPART) by 25 November 2022 of its intention to make application for an SRV in respect of the 2023/24 financial year. The SRV would be spread across the first four years of the LTFP for 2023/24 to 2032/33 in the following manner:

· An 8.5% increase for 2023/24 (inclusive of the 3.7% rate peg determined by IPART for that year)

· A 7.5% increase for 2024/25 (inclusive of the forecast rate peg of 3.5% for that year)

· A 6.5% increase for 2025/26 (inclusive of the forecast rate peg of 3.0% for that year)

· A 5.5% increase for 2026/27 (inclusive of the forecast rate peg of 2.5% for that year)

3. Council adopt the LTFP for 2023/24 to 2032/33.

4. Council note the purpose of the SRV is to address the ongoing resilience of Council’s capacity to support its community through the continuation of current services (financial sustainability), long term sustainable management of community assets and the implementation of several strategic initiatives.

5. Council progress its SRV application such that it is completed and submitted to IPART by the due date of 3 February 2023.

6. Subject to the approval of the SRV application by IPART, Council increase its pensioner rate concession by $50, to $300 per annum, commencing from the 2023/24 financial year.

7. Council review its Hardship Policy prior to the adoption of the 2023/24 Delivery Program and Budget.

Corporate Support Division

Nil

Community and Environment Division

Nil

Planning and Compliance Division

Nil

Infrastructure and Major Projects Division

Nil

PUBLIC FORUM – NON AGENDA ITEMS

Questions with Notice

Notices of Motion

SUPPLEMENTARY AGENDA

MATTERS OF URGENCY

General Manager's Report No. GM34/22

Office of the General Manager

Date of Meeting: 23/11/2022

1 ADOPTION OF A DRAFT LONG TERM FINANCIAL PLAN FOR 2023/24 – 2032/33 AND PROGRESSION OF A SPECIAL RATE VARIATION APPLICATION FOR 2023/24

EXECUTIVE SUMMARY

· Successive versions of Council’s Long Term Financial Plan (LTFP) have noted that Council’s financial capacity began to decline after the 2016 boundary adjustment with the City of Parramatta Council. In addition to the financial impact of the boundary adjustment, Council’s financial capacity has continued to decline due to a rate peg that does not adequately reflect the increasing costs of servicing the community; cost shifting from State and Federal Governments; the cost impacts of increasingly frequent natural disasters; the COVID pandemic; and, more recently, the significant inflationary pressures that the entire community is facing.

· With a continuous focus on ongoing and one-off measures that have successfully reduced costs over an extended period, Council, unlike a majority of councils across NSW, has been able to avoid seeking a Special Rate Variation (SRV) for more than a decade. Council has now concluded that action is required through the submission of a SRV application to the Independent Pricing and Regulatory Tribunal (IPART) to ensure that recurrent services, including allocating appropriate budgets for asset maintenance and renewal, can be provided in a sustainable manner into the future. Without action, Council’s forecast deficit from normal operations will, by 2033, exceed $8 million.

· Office of Local Government (OLG) Guidelines clearly state that the criteria against which IPART will assess an SRV application are based on what Council is required to do under Integrated Planning and Reporting (IP&R) requirements. In this regard, the need for, and purpose of, a different revenue path for the Council’s General Fund (as requested through an SRV) needs to be clearly articulated and identified in Council’s IP&R documents, in particular its Delivery Program, LTFP and Asset Management Plans.

· Having regard to the above, Council indicated support to prepare a proposal to progress investigations for an SRV to ensure Council is financially sustainable and to engage with the community about the need for this approach. Council also sought to understand the opportunities to deliver on community priorities that cannot be delivered within existing resources.

· In order to meet the requirements in the OLG Guidelines, a draft LTFP for 2023/24 – 2032/33 was prepared which incorporates a Baseline scenario – providing forecasts for General Fund revenue and expenditure in a business-as-usual mode (i.e. exclusive of any SRV income and related expenditure); and a Special Variation scenario – providing forecasts for General Fund revenue and expenditure incorporating the proposed SRV in full and the related expenditure which is to be funded by the SRV.

· The Special Variation scenario included in the draft LTFP for 2023/24 – 2032/33 indicated that a 28% (31.05% cumulative) SRV was required to provide sufficient financial capacity for Council to fund each of the items identified in the LTFP’s Special Variation scenario. To assist the community in managing such an increase, it was proposed that the SRV would be spread across the first four years of the 2023/24 – 2032/33 LTFP.

· A Community Engagement Action Plan was developed to outline the approach, purpose and goals, development of key messages and the timeline for community consultation on a potential SRV application. The Plan was developed to ensure that Council meets the SRV assessment criteria set out by the OLG and IPART.

· Following a decision at its 28 September 2022 Meeting, Council has progressed the SRV process in line with the Community Engagement Action Plan and the supporting SRV Background Paper and Assessment of Capacity to Pay Report.

· Council is now in receipt of the Community Engagement Outcomes Report prepared by Morrison Low which details the thorough engagement process undertaken between 4 October and 8 November. The Outcomes Report indicates that the main issues raised through submissions are:

o The SRV increase is too high and the timing is difficult having regard to cost of living pressures, inflation, interest rates, economic conditions, energy bills, rent rises and mortgages

o Council should increase efficiencies, increase productivity or savings, reduce wastage, reduce overhead costs

o The SRV will have a harder impact on retirees, pensioners, the elderly

o There is an understanding and awareness that Council is facing rising prices

o Development growth in the Shire should be providing enough income for Council

o Council should prioritise essential projects (not wish list) or defer non-essential projects

o Council should tighten its belt – live within its means – or just focus on Council’s essential services

o Council should undertake better financial management

o Council is out of step with the community

o There is dissatisfaction with current levels of maintenance, services, facilities, planning, traffic, overdevelopment, congestion (waste, roads, pathways, parks, trees, stormwater, public amenities, etc)

o The SRV rate increase should not be above the CPI, inflation, wage growth or the IPART rate.

· It is acknowledged that the majority of feedback received argues against Council proceeding with a SRV, or at least proceeding with a smaller SRV. What is also evident is that where Council has had the opportunity to fully articulate the background and necessity of the SRV, the community’s response is generally more positive. In particular, engagement with organisations that have frequent and ongoing contact with Council and, therefore, arguably a deeper understanding of Council’s activities, has been significantly more positive.

· The current economic environment is challenging with recent recognition that inflation is currently at or close to 8%. These are challenging times for many in the community and whilst Council has no desire to add to current pressures, it is evident that there is never an opportune time to address the financial imbalance. The last few years have been characterised by a global pandemic, various natural disasters and the current global outlook is uncertain, at least in the short term.

· Against this scenario is the opportunity to address the ongoing resilience of Council’s capacity to support its community through the continuation of current services, long term sustainable management of community assets and the implementation of several strategic initiatives. In particular, issues around the maintenance of Council assets will only become more expensive over time forcing the community to pay significantly more than what is currently proposed.

· Though most of the issues raised from the engagement were canvassed in a set of Questions and Answers (Q&As) published on Council’s website during the public exhibition period, Councillors and staff have subsequently discussed the issues of pensioner rate rebates and Council’s Hardship Policy to determine what assistance may be able to be provided to those who may find it difficult to pay the SRV increase. Based on those discussions, it is proposed that Council’s current pensioner rate rebate to eligible pensioners be increased by $50 to $300 per annum (subject to an approved SRV) and the Hardship Policy be reviewed prior to the adoption of the 2023/24 Delivery Program and Budget.

· Noting all of the above, it is apparent that Council has the following options to consider:

o Advise IPART of Council’s intention to make application for a SRV in respect of the 2023/24 financial year in line with what was proposed during the public exhibition process; and subject to the amendments proposed in this Report, adopt the LTFP for 2023/24 to 2032/33.

o Not progress an application to IPART for a SRV in respect of the 2023/24 financial year; and request the General Manager to urgently prepare a new draft LTFP for 2023/24 to 2032/33 which takes account of the impact on normal operations, asset management, major capital projects, strategic initiatives and Council’s financial sustainability measures into the future (including the achievement of annual balanced budgets) of not progressing the SRV application.

· If Council decides not to progress an SRV application, it needs to be cognisant of the following financial impacts on its operations:

o Normal Operations – there will be insufficient financial capacity to fund the continuance of normal operations into the future

o Asset Management – there will be insufficient capacity to fund the requirements identified in Council’s Asset Management Plans to ensure maintenance of the assets in a satisfactory condition

o Major Capital Projects – there will be insufficient capacity to fund the recurrent cost of operating major new capital projects once construction is complete. This includes Hornsby Park and Westleigh Park

o Strategic Initiatives – without an increase in Council’s financial capacity, funding is unlikely to be available to fund the 14 key strategic initiatives proposed in the SRV.

· To ensure Council’s future financial sustainability and the maintenance of services and assets to the level desired by the community, the first of the two options provided above is recommended.

|

THAT: 1. The contents of General Manager’s Report No. GM34/22 and Morrison Low’s Community Engagement Outcomes Report, which provide details of the outcome of the public exhibition process conducted between 4 October 2022 and 8 November 2022 in respect of Council’s draft Long Term Financial Plan (LTFP) for 2023/24 to 2032/33 and Council’s intention to make application for a Special Rate Variation (SRV) for the 2023/24 financial year, be received and noted. 2. Council advise the Independent Pricing and Regulatory Tribunal (IPART) by 25 November 2022 of its intention to make application for an SRV in respect of the 2023/24 financial year. The SRV would be spread across the first four years of the LTFP for 2023/24 to 2032/33 in the following manner: · An 8.5% increase for 2023/24 (inclusive of the 3.7% rate peg determined by IPART for that year) · A 7.5% increase for 2024/25 (inclusive of the forecast rate peg of 3.5% for that year) · A 6.5% increase for 2025/26 (inclusive of the forecast rate peg of 3.0% for that year) · A 5.5% increase for 2026/27 (inclusive of the forecast rate peg of 2.5% for that year) 3. Council adopt the LTFP for 2023/24 to 2032/33. 4. Council note the purpose of the SRV is to address the ongoing resilience of Council’s capacity to support its community through the continuation of current services (financial sustainability), long term sustainable management of community assets and the implementation of several strategic initiatives. 5. Council progress its SRV application such that it is completed and submitted to IPART by the due date of 3 February 2023. 6. Subject to the approval of the SRV application by IPART, Council increase its pensioner rate concession by $50, to $300 per annum, commencing from the 2023/24 financial year. 7. Council review its Hardship Policy prior to the adoption of the 2023/24 Delivery Program and Budget. |

PURPOSE

The purpose of this Report is to provide Council with the background and details of the community consultation undertaken between 4 October and 8 November 2022 in respect of the draft LTFP for 2023/24 – 2032/33 and the proposal for Council to submit an SRV application to IPART for the 2023/24 financial year.

BACKGROUND

Successive versions of Council’s LTFP have noted that Council’s financial capacity began to decline after the 2016 boundary adjustment with the City of Parramatta Council, which significantly impacted Council’s Income Statement results and Annual Budget. In addition to the financial impact of the boundary adjustment, Council’s financial capacity has continued to decline due to a rate peg that does not adequately reflect the increasing costs of servicing the community; cost shifting from State and Federal Governments; the cost impacts of increasingly frequent natural disasters; the COVID pandemic; and, more recently, the significant inflationary pressures that the entire community is facing.

With a continuous focus on ongoing and one-off measures that have successfully reduced costs over an extended period, Council, unlike a majority of councils across NSW, has been able to avoid seeking an SRV for more than a decade. Following careful consideration over many months in workshops and through formal reporting, Council has concluded that action is now required through the submission of an SRV application to IPART to ensure that recurrent services, including allocating appropriate budgets for asset maintenance and renewal, can be provided in a sustainable manner into the future. Without action, Council’s forecast deficit from normal operations will, by 2033, exceed $8 million.

OLG Guidelines

The OLG’s Guidelines for the Preparation of an Application for a Special Variation to General Income indicate that when IPART assesses an application for a SRV, it will examine the extent to which Council has fulfilled its obligations under IP&R requirements. In this regard, it is important for Council to be able to link community outcomes and aspirations (as identified in the Community Strategic Plan) to key actions in the Delivery Program, as well as ensuring that appropriate resources are available at the right time as outlined in Council’s Resourcing Strategy.

The Guidelines state that the criteria against which IPART will assess an SRV application are based on what Council is required to do under IP&R i.e.:

The need for, and purpose of, a different revenue path for the council’s General Fund (as requested through the special variation) is clearly articulated and identified in the council’s IP&R documents, in particular its Delivery Program, Long Term Financial Plan and Asset Management Plan where appropriate. In establishing need for the special variation, the relevant IP&R documents should canvas alternatives to the rate rise. In demonstrating this need councils must indicate the financial impact in their LTFP applying the following two scenarios:

· Baseline scenario – General Fund revenue and expenditure forecasts which reflect the business as usual model, and exclude the special variation, and

· Special Variation scenario – the result of implementing the special variation in full is shown and reflected in the General Fund revenue forecast with the additional expenditure levels intended to be funded by the special variation.

The IP&R documents and the council’s application should provide evidence to establish this criterion. This could include evidence of community need/desire for service levels/project and limited council resourcing alternatives. Evidence could also include analysis of council’s financial sustainability conducted by Government agencies. In assessing this criteria, IPART will also take into account whether and to what extent a council has decided not to apply the full percentage increases available to it in one or more previous years under section 511 of the Local Government Act. If a council has a large amount of revenue yet to be caught up over the next several years, it should explain in its application how that impacts on its need for the special variation.

Evidence that the community is aware of the need for and extent of a rate rise. The Delivery Program and LTFP should clearly set out the extent of the General Fund rate rise under the special variation. In particular, councils need to communicate the full cumulative increase of the proposed SV in percentage terms, and the total increase in dollar terms for the average ratepayer, by rating category. Council should include an overview of its ongoing efficiency measures and briefly discuss its progress against these measures, in its explanation of the need for the proposed SV. Council’s community engagement strategy for the special variation must demonstrate an appropriate variety of engagement methods to ensure community awareness and input occur. The IPART fact sheet includes guidance to councils on the community awareness and engagement criterion for special variations.

The impact on affected ratepayers must be reasonable, having regard to both the current rate levels, existing ratepayer base and the proposed purpose of the variation. The council’s Delivery Program and LTFP should:

· Clearly show the impact of any rate rises upon the community,

· Demonstrate the council’s consideration of the community’s capacity and willingness to pay rates, and

· Establish that the proposed rate increases are affordable having regard to the community’s capacity to pay.

In assessing the impact, IPART may also consider

· Socio-Economic Indexes for Areas (SEIFA) data for the council area; and

· Whether and to what extent a council has decided not to apply the full percentage increases available to it in one or more previous years under section 511 of the Local Government Act.

The relevant IP&R documents must be exhibited (where required), approved and adopted by the council before the council applies to IPART for a special variation to its general income. It is expected that councils will hold an extraordinary meeting if required to adopt the relevant IP&R documents before the deadline for special variation applications.

The IP&R documents or the council’s application must explain and quantify the productivity improvements and cost containment strategies the council has realised in past years and plans to realise over the proposed special variation period. Councils should present their productivity improvements and cost containment strategies in the context of ongoing efficiency measures and indicate if the estimated financial impact of the ongoing efficiency measures have been incorporated in the council’s Long Term Financial Plan.

Any other matter that IPART considers relevant. The criteria for all types of special variation are the same. However, the magnitude or extent of evidence required for assessment of the criteria is a matter for IPART.

_______________________________

Long Term Financial Plans (LTFP)

The preparation by Council of a LTFP is a requirement under the IP&R framework for NSW Local Government and forms part of Council’s Resourcing Strategy. The LTFP must be for a minimum of 10 years and make clear the financial direction of Council as well as the impact of that direction on achieving community priorities.

The main purpose of the LTFP is to guide and inform decision-making in respect to Council’s financial sustainability and to ensure that Council has sufficient financial resources to fund asset maintenance and renewal and provide services to the standard that the community expects. The LTFP establishes the framework for sound financial decisions and provides an insight as to the financial sustainability of the Council over the planning period of the document. The key objectives in developing the LTFP are:

· To achieve balanced budgets and income statement results that provide sufficient capacity to respond to budget ‘shocks’ as they arise

· To maintain into the future a level of service that the community has come to expect

· To ensure that assets provided by Council are designed and funded to meet a defined level of demand and/or need of the community

· To achieve continuous financial improvement

· To only use external loan borrowing when Council’s financial capacity and operating performance allow

· To achieve/maintain financial sustainability benchmarks (i.e. indicators prescribed by the OLG).

Successive versions of Council’s LTFP have noted that Council’s financial capacity began to decline after the 2016 boundary adjustment with the City of Parramatta Council, significantly impacting Council’s Income Statement results and Annual Budget. In the period since the boundary adjustment, Council’s financial capacity has continued to reduce because of internal and external factors, notably: an increase in the Emergency Services Levy payable to the NSW State Government of $1 million per year; the need to provide a recurrent budget for Council’s largest project, Hornsby Park; the need to provide additional funding to meet the requirements identified in Council’s revised Asset Management Plans; the need to implement strategic plans to cater for a growing population; and an increase in statutory employee superannuation to 12%, amounting to $1.2 million in additional payments each year from 2026.

After accounting for these additional expenditure items in LTFPs, Council concluded that its forecast financial capacity is below acceptable levels and action is required to ensure that recurrent services, including allocating appropriate budgets for asset maintenance and renewal could be provided in a sustainable manner into the future.

LTFP for 2022/23 – 2031/32

The LTFP for 2022/23 – 2031/32 was adopted by Council on 13 July 2022. It made clear the financial position of Council over the next 10 years in respect to maintaining current service levels (which has been Council’s policy position since the 2016 boundary change), maintaining assets to the condition required by the community and delivering strategic initiatives agreed to by Councillors. The LTFP indicated a decline in financial position below acceptable levels against industry benchmarks over the term of the LTFP. It was noted that this projected decline in financial position will be put under further pressure from issues such as:

· Construction and supply chain issues resulting in significant cost escalations across capital projects

· Cost shifting from other tiers of government and statutory levies that exceed reasonable CPI based increases

· The finalisation of an external independent assessment of the major asset classes – roads, drainage, buildings and open space – identifying in excess of $3 million per annum needed to maintain these assets to a reasonable condition

· Potential changes released in a draft report by IPART into the review of Domestic Waste Management Services that, if approved, may result in a significant financial impost on Council’s budget estimated at $2.3 million.

· The cost impacts of increasingly frequent natural disasters e.g. Council has identified in excess of $3 million of damage to Council’s road pavements as a result of flooding and the extraordinarily high volume of rain experienced over the last 12 months

· Increased employee costs due to Award increases and labour shortages.

Having regard to a declining financial position and the above issues, a range of actions were outlined in the 2022/23 – 2031/32 LTFP as potential measures to improve Council’s future financial sustainability. These actions included:

· The need for a SRV to rebalance Council’s finances within acceptable levels over the long term. Priority should be given to meeting asset management requirements and ensuring there is sufficient funding for recurrent services. An SRV is recommended in the first instance because of the quantum of funds required to provide balanced budgets. Other funding initiatives such as the generation of additional income from increases to user fees and charges should, however, be explored and implemented to potentially reduce the size of an SRV required

· Carefully assessing whether there is value in creating any further strategic documents given unfunded initiatives in existing documents require at least $8.8 million of funding (based on preliminary costing for only 50% of the actions identified)

· Continuing with Council’s previously agreed position of developing Hornsby Park ahead of Westleigh Park (and reinforcing this messaging with the community). To mitigate financial risk, works at Westleigh Park should not be undertaken until it is financially appropriate to commence. The development of Westleigh Park also requires a recurrent budget for operations and asset maintenance and renewal expenditure to be identified

· Communicating to the community the scope of works that can realistically be completed at Hornsby Park in the early stages of the life of this Park and how this may differ in regard to the full scope of the Master Plan

· Carefully considering the acceptance of further external grants for capital purposes. There is insufficient capacity within the LTFP to fund the associated recurrent costs from any new capital that is not already included in the LTFP. It may be in Council’s best financial interests to decline capital grant funding depending on whether an evidence-based need for the project exists within Council’s strategic documents and depending on the availability of budgets to fund recurrent costs

· Reviewing other income streams such as fees and charges to ensure appropriate price setting and assessing whether price increases could be used to generate additional income

· Continuing a freeze on Council’s approved Full Time Equivalent headcount where appropriate; with no new positions to be created unless offset by an equivalent position elsewhere or specific new funding

· Maintaining cost increases to modest levels in regard to non-labour related expenses each year

· Continuing with financial improvement initiatives (the development of business improvement plans and service reviews)

· Considering whether there is a case to rationalise underutilised assets to reduce ongoing cost requirements and/or provide one off capital funding from sale proceeds towards other capital investment decisions.

LTFP for 2023/24 – 2032/33

Following the adoption of the 2022/23 – 2031/32 LTFP, a number of matters identified in the Plan progressed to a point whereby a further review of the LTFP document was required e.g.:

· External Economic Environment – the external economic environment has changed following recovery from the COVID-19 pandemic. Consumer Price Index (CPI) growth has exceeded earlier projections, which has placed pressure on many of Council’s budgets. The Wages Price Index is also forecast to increase to a greater extent over the next 10 years compared to earlier predictions.

· Asset Management Strategy – the rising costs referred to above have required a revision of the 10-year expenditure projections in Council’s updated Asset Management Strategy. As a consequence, the latest Strategy, which was received and noted by Council at its 11 May 2022 Meeting, was revised into a 2023/24 – 2032/33 document to account for the additional funding required to maintain assets to the standard desired by the community.

· Strategic Initiatives – the 2022/23 – 2031/32 LTFP noted the existence of a number of initiatives across 36 strategic and technical documents previously adopted by Council that could not be funded because of insufficient financial capacity over the term of the LTFP (noting that some of the recommendations in these documents are responding to State legislative requirements which need to be progressed e.g. Housing Supply and Diversity). During a series of workshops, Councillors considered whether strategic initiatives desired by the community could be progressed if funding could be provided (at least in part) through an SRV. Regard was given to feedback received from the community through numerous surveys over the past three years and this led to the identification of 14 key initiatives which could be achieved or progressed in the next 10 years.

· Special Rate Variation – workshops were held with Councillors to discuss the need for an SRV to ensure Council’s finances are rebalanced within acceptable levels into the future. Following these workshops, Councillors indicated support to prepare a proposal for an SRV to ensure Council is financially sustainable and to engage with the community about the need for this approach. Council also sought to understand the opportunities to deliver on community priorities that cannot be delivered within existing resources. As a consequence, a revision of the 2022/23 – 2031/32 LTFP was required to calculate the size of the SRV required and to ensure that all of the IP&R requirements of an SRV are met.

In addition to the above, Council also wanted to maintain its strong commitment to adopting annually a balanced budget and that its Income Statement results meet financially acceptable benchmarks. This includes an annual Operating Performance Ratio (OPR) that is in the range of 2-4% to enable Council to respond in a timely manner towards infrastructure assets that may fail, the impact of natural disasters on local service provision and clean-ups and cost shifting from other tiers of government.

It is financially prudent to target an acceptable OPR to respond to one off budget shocks that can occur over the course of the year and not affect the normal continuance of service provision. Council’s major reasons for targeting a 2-4% OPR include its past experiences with:

· Capital project cost escalations – natural disasters, rising construction costs and supply shortages following economic recovery from the COVID-19 pandemic have placed pressure on Council’s construction budgets. Recent annual budgets have been impacted by the need to provide additional allocations to the Wisemans Ferry Boat Ramp project and Galston Aquatic & Leisure Centre remediation project.

· Investment income returns – investment returns have fluctuated during the COVID-19 pandemic with the majority of Council’s investment products linked to the base rate set by the Reserve Bank of Australia. When the base rate was reduced to 0.1%, Council’s budget for investment income was reduced significantly.

· Natural disasters – the Shire has been impacted by multiple severe weather events that were declared natural disasters by the NSW Government between 2018 and 2022. Each of these events typically costs Council several hundreds of thousands of dollars in clean-up costs that are not always able to be recouped from the NSW Government. A key issue that recent natural disasters has created is that even when a proportion of Council’s expenditure on clean up and recovery can be recouped, Council can wait several years for reimbursement.

· Workplace of the future – Since the discovery of asbestos in Council’s Administration Centre based in Hornsby, Council staff have predominantly worked from a temporary office location in Thornleigh. While the cost of leasing these premises has been included in LTFPs for the next five years, there is a long-term need for Council to resolve office accommodation needs that will require funding beyond this point. Unexpected remediation work undertaken to date at the Hornsby Administration Centre has adversely impacted Council’s budget by $1.53 million.

· Asset Management – Asset Management Plans have been revised for 95% of Council’s depreciable asset base including all roads, stormwater drainage, buildings and open space assets to be maintained at the level desired by the community. However, Asset Management Plans for the remaining 5% of Council’s depreciable assets comprising foreshores and some other structures are still being prepared and the funding requirements are not yet available.

· State Government Costs – There are some costs over which Council has no control such as levies charged by the NSW Government. As an example, over recent years, the Emergency Services Levy payable to the State has increased by more than $1 million and in the order of 40%, which is above the level of estimated increases (CPI) in previous LTFPs. (N.B. The growth in rates income as allowed through rate pegging does not keep pace with such increased costs).

In line with the above, an updated draft LTFP for 2023/24 – 2032/33 was prepared which incorporates the following two scenarios required by the OLG’s Guidelines:

· Baseline scenario – which provides forecasts for General Fund revenue and expenditure in a business-as-usual mode (i.e. exclusive of any SRV income and related expenditure)

· Special Variation scenario – which provides forecasts for General Fund revenue and expenditure incorporating the proposed SRV in full and the related expenditure which is to be funded by the SRV.

The Baseline scenario includes forecast income and expenditure associated with:

· The normal continuance of services, representing costs associated with the ongoing provision of Council’s current service offerings into the future

· The required recurrent costs to operate Council’s largest project, Hornsby Park, once construction is complete (i.e. $3.1 million per year from 2028)

· The forecast funding requirements identified in Council’s updated Asset Management Strategy (i.e. an additional $4.1 million per year).

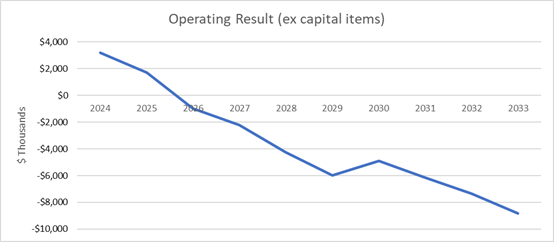

The financial results associated with the Baseline scenario are similar to the results from the adopted 2022/23 – 2031/32 LTFP. The Income Statement over the 10-year period forecasts a deficit for eight out of the 10 years, with an average deficit of $3.582 million per annum. Concurrently, a negative OPR is forecast for eight out of the 10 years. This is below the benchmark set by the OLG and also below Council’s internally-set minimum benchmark of 2-4% which it uses to protect annual budgets against unexpected budget shocks that typically occur.

The scenario indicates that the forecast recurrent budget deficits would most likely result in the use of unrestricted cash, and this would ultimately have significant ramifications for Council’s continued operation e.g. limiting the ability of Council to pay creditors as and when they fall due. In overall terms, the Baseline scenario concludes that Council’s forecast financial capacity is below acceptable levels and action is required to improve its future financial direction.

The Special Variation scenario includes forecast income and expenditure associated with:

· All income and expenditure from the Baseline scenario i.e. the normal continuance of services; the $3.1 million of recurrent funding required for Hornsby Park from 2028; and the $4.1 million funding gap identified in Council’s updated Asset Management Strategy.

· The funding of the 14 key initiatives identified (based on community feedback) to be achieved or progressed in the next 10 years – i.e. an expenditure of an extra $67.26 million across the 10-year period.

· Maintaining sufficient financial capacity to provide an OPR of at least 2% per year to protect annual budgets against unexpected budget shocks that typically occur.

The Special Variation scenario indicates that a 28% (31.05% cumulative) SRV would be required to provide sufficient financial capacity for Council to fund each of the items identified above. To assist the community in managing such an increase, the LTFP proposes that the SRV be spread across the first four years of the 2023/24 – 2032/33 LTFP (i.e. rate increases of 8.5% for 2023/24, 7.5% for 2024/25, 6.5% for 2025/26 and 5.5% for 2026/27), noting that this is inclusive of the forecast rate peg over this same period of 3.9% for 2023/24, 3.5% for 2024/25, 3.0% for 2025/26 and 2.5% for 2026/27.

The financial results associated with the Special Variation scenario show that the Income Statement would be in surplus for the 10-year period and that the average surplus would be $6.584 million per annum. Concurrently, the OPR forecast averages 3.55% for the 10-year period, which is above the benchmark set by the OLG and meets Council’s internally-set minimum benchmark over the life of the Plan.

The Balance Sheet results over the 10-year period maintain equity, liabilities and non-current assets within acceptable levels and each of the ratios that are based on the primary financial statements would also be above acceptable benchmarks i.e. the OPR, Own Source Operating Revenue Ratio, Unrestricted Current Ratio and the Debt Service Cover Ratio. Infrastructure asset ratios would also be acceptable even though the Asset Maintenance Ratio of 97% falls slightly below the benchmark of 100% – this is particularly relevant noting that Asset Management Plans for Foreshore Assets and Other Structures are yet to be finalised.

In overall terms, the Special Variation scenario indicates that an SRV of 28% over the first four years of the 2023/24 LTFP (31.05% cumulative) is sufficient to rebalance Council’s projected finances and maintain financial benchmarks set by the OLG and Council. The draft LTFP concludes it is appropriate that:

· Council make application to IPART for a 28% SRV inclusive of the rate peg amount (31.05% cumulative) over the first four years of the 2023/24 – 2032/33 LTFP

· Council reviews other income streams such as fees and charges (noting that a number are prescribed by legislation and are unable to be increased by Council) to ensure appropriate price setting and to assess whether price increases could be used to generate additional income

· No new staff positions to be created as appropriate unless offset by an equivalent position elsewhere, or grant funded or income-generating positions

· Council maintains cost increases to modest levels with regards to non-labour related expenses each year, excluding the additional allowances that have been made in the LTFP including annual allocations for asset management and strategic initiatives

· No new loan borrowing be undertaken by Council unless financial capacity above a 2% budget surplus/operating performance ratio is available each year in the Plan

· Council continues financial improvement initiatives through the development of business improvement plans

· Council considers whether there is a case to rationalise underutilised assets to reduce ongoing cost requirements and/or provide one off capital funding from sale proceeds towards other capital investment decisions.

The draft LTFP indicates that if Council decides not to progress an SRV application, it needs to be cognisant of the following financial impacts on its operations:

· Normal Operations – there will be insufficient financial capacity to fund the continuance of normal operations into the future. Additional funding will need to be identified to fund forecast deficits or services may need to be reduced to ensure a balanced budget each year. Without action, budget reductions will be required that will reduce levels of service such as through the closure of facilities or reduction in hours of operation.

· Asset Management – there will be insufficient capacity to fund the requirements identified in Council’s Asset Management Plans to ensure maintenance of the assets in a satisfactory condition. As a result, the condition of Council’s assets will be expected to decline, and the level of infrastructure backlog will increase unless alternative funding can be identified.

· Major Capital Projects – there will be insufficient capacity to fund the recurrent cost of operating major new capital projects once construction is complete. This includes Hornsby Park and Westleigh Park, noting that the capital construction of these projects is partly funded from external sources such as the NSW Stronger Communities Fund and Development Contributions. If funding is not provided, future versions of the LTFP will likely recommend that projects are paused until a funding source can be identified.

· Strategic Initiatives – without an increase in Council’s financial capacity, no funding will be available to fund key strategic initiatives. This poses a risk in that Council may not be able to fulfill legislative requirements in respect of some actions in strategic plans or respond to long-held priorities of the Hornsby Shire community. Specific measures include Council’s obligations under the Hornsby Kuring-gai Bushfire Risk Management Plan and Council commitments under the Social Inclusion Hornsby (Disability Inclusion Action Plan) 2021-2025.

_______________________________

28 September 2022 Council Resolution

At the 28 September 2022 Workshop Meeting, Council considered General Manager’s Report No. GM31/22 – Adoption of a Draft Long Term Financial Plan for 2023/24 – 2032/33 and Progression of a Special Rate Variation Application for 2023/24 and resolved that:

1. Council provide advice to the community of its intention to make application to the Independent Pricing and Regulatory Tribunal (IPART) for a Special Rate Variation (SRV) in respect of the 2023/24 financial year.

2. Council note that the draft Long Term Financial Plan (LTFP) for 2023/24 – 2032-33 attached to General Manager’s Report No. GM31/22 incorporates the latest data from the Asset Management Strategy for 2023/24 – 2032/33 in respect of the maintenance of Council assets to the standard desired by the community; and, in accordance with Office of Local Government Guidelines, incorporates a Baseline scenario (which provides forecasts for General Fund revenue and expenditure in a business-as-usual mode); and a Special Variation scenario (which provides forecasts for General Fund revenue and expenditure incorporating the proposed SRV in full and the related expenditure which is proposed to be funded by the SRV).

3. Council adopt the draft LTFP for 2023/24 – 2032/33 attached to General Manager’s Report No. GM31/22 and place the document on public exhibition.

4. Following the public exhibition, and before 23 November 2022, a further report be prepared for Council’s consideration which outlines and responds to any submissions received during the exhibition period.

5. The Report referred to in 4. above, is to also make an appropriate recommendation in respect of the progression of a SRV application to IPART.

6. The Special Rate Variation Community Engagement Action Plan and its supporting documents (an SRV Background Paper and an Assessment of Capacity to Pay Report) attached to General Manager’s Report No. GM31/22 be endorsed, noting that their purpose is to assist in the seeking of community feedback in relation to Council’s intent to make application to IPART for a SRV in respect of the 2023/24 financial year.

DISCUSSION

The OLG’s Guidelines clearly state that the criteria against which IPART will assess an SRV application are based on what Council is required to do under IP&R. In this regard, the need for, and purpose of, a different revenue path for the council’s General Fund (as requested through an SRV) needs to be clearly articulated and identified in Council’s IP&R documents, in particular its Delivery Program, LTFP and Asset Management Plans.

Council’s current suite of IP&R documents include the Community Strategic Plan Your Vision | Your Future for 2022-2032; Delivery Program for 2022-2026; Operational Plan for 2022/23; draft LTFP for 2023/24 – 2032/33; Asset Management Strategy for 2023/24 – 2032/33; and Workforce Management Plan for 2022/23 – 2025/26.

Community Strategic Plan for 2022-2032, Delivery Program for 2022-2026 and Operational Plan for 2022/23

Following extensive community consultation, Council endorsed its 10-year Community Strategic Plan, Your vision | Your future 2032, on 8 June 2022. Developed in partnership with the community, the Community Strategic Plan is the highest-level plan that Council prepares. It identifies the main priorities and aspirations for Hornsby Shire and identifies the strategic direction for where the people of Hornsby Shire want to be in 2032.

Council's response to the Community Strategic Plan, the Delivery Program for 2022-2026 and Operational Plan for 2022/23, were adopted on 29 June 2022 and are the blueprint for achieving the community's agenda for the next 12 months specifically and more generally over the course of Council's term of office. As well as outlining priorities, planned capital projects, budget and other financial details including resourcing information, information on rating and domestic waste management relating to 2022/23 are included.

When adopting the Delivery Program, Council noted that operating deficits will occur over the term of the Program if there is a normal continuance of services to the level that the community has come to expect. It was noted that these operating deficits did not take into account the asset management gap detailed in the draft 2022/23 – 2031/32 LTFP which was submitted to the 11 May 2022 General Meeting (for the purpose of public exhibition) but which was only part way through that public exhibition when the Delivery Program was adopted.

Asset Management Strategy for 2023/24 – 2032/33

As noted earlier, the external economic environment has changed following recovery from the COVID-19 pandemic. CPI growth has exceeded earlier projection, and this has placed pressure on many of Council’s budgets. The Wages Price Index is also forecast to increase to a greater extent over the next 10 years compared to earlier predictions. These rising costs required a revision of 10-year expenditure projections.

The latest Asset Management Strategy (for 2023/24 – 2032/33) was endorsed by Council at its 28 September 2022 General Meeting and accounts for the additional funding required to maintain assets to the standard desired by the community.

In assessing the cost of maintaining Council’s depreciable infrastructure asset base, the assets were separated into four categories – buildings; drainage; open spaces; and roads and transport. For each category, data was collated on the assets Council owns. External contractors were engaged to assist in verifying the accuracy of Council’s data and community survey results were used as a source to inform desired levels of service for the categories. This led to Council’s determination of an appropriate standard for each asset category.

Using this data, the expected costs to maintain and renew our existing asset base to a satisfactory standard over the next 10 years were calculated and compared to recurrent budget funding allocations. This resulted in the calculation of a funding gap across all four asset categories. There was also a need to factor in the forecast maintenance and renewal requirements of new assets that are expected to be built over the next 10 years, assuming the funding for the construction of these assets is confirmed.

The 2023/24 – 2032/33 Strategy highlights that to achieve community desired service levels and to maintain required technical service levels, there is a deficit (shortfall) of $4.1 million per year on average across the four asset categories over the 10 years of the draft 2023/24 – 2032/33 LTFP. This represents just over 0.2% of the gross replacement cost of Council’s asset base of approximately $2 billion.

The consequences of Council not being able to provide adequate funding for the maintenance of its assets are:

· Deteriorating quality of existing assets (e.g. reduction in road network condition)

· Inability to renew ageing assets

· Inability to adequately maintain newly constructed assets

· Not meeting desired service levels expected by our local community.

· A shift to reactive maintenance (i.e. responding to asset failures as they occur) rather than proactively managing assets in line with community expectations. Ultimately, this will transfer a significantly increased cost to future generations of maintaining the assets properly.

Workforce Management Plan for 2022/23 – 2025/26

The Workforce Management Plan is a mandatory requirement under the IP&R framework and is intended to address the human resourcing requirements of Council’s Delivery Program. It was developed by Council to ensure it has the capacity and capability to deliver on its goals and objectives over the period of the Plan. It takes account of the anticipated workload drivers over the timeframe including the delivery of a number of major works projects and the evolving nature of the work environment in response to the COVID-19 pandemic.

The Plan includes a snapshot of the current workforce, demographics of the Hornsby community and an employment proposition that reflects the workforce Council seeks to retain and attract. It considers external and internal trends and how Council might respond to these drivers of change in the future. The strategic objectives and corresponding actions and measures clearly articulate what is needed to attract and retain the workforce requirements of Council.

The document excludes processes which are part of human resource services, instead identifying a suite of carefully developed strategies that address external pressures and underlying challenges for Council. Alongside the strategic objectives and actions in the Plan, Council will continue to deliver key operational human resource functions, including performance management, remuneration framework, recruitment, learning and development, health and safety, grievance management, and employee and industrial relations.

The Plan will guide Council’s overall approach to recruitment, staff progression and development, and succession planning. It is a practical and live document which will be used by all executives, managers and supervisors within Council. The Plan is integrated in the IP&R process, with progress measures drawing on our staff engagement and community satisfaction feedback processes. Importantly, the document is regularly monitored and adjusted when required in response to new workforce challenges.

Strategic Initiatives

Over recent years, Council has undertaken a series of technical and evidence-based strategies to formulate initiatives required to deliver services to the community for each of Council’s unique disciplines. Thirty-six different strategies and technical documents have been adopted by Council.

A range of strategic initiatives are identified across the documents, some of which can be funded within existing budgets, and some are likely to attract funding such as from external grants or from the generation of additional income. However, there are a number of unfunded initiatives across the strategies, many of which have been identified as high priority but have no funding source.

Due to deficits being forecast in eight out of ten years in the Baseline scenario of the draft 2023/24 – 2032/33 LTFP, there is insufficient financial capacity to fund the unfunded initiatives identified unless additional income is generated, such as through an SRV, which could be linked to the funding of specific initiatives.

In order to select unfunded initiatives for inclusion in an SRV application, Council carefully considered feedback from the community through the results of the Community Strategic Plan, Your vision | Your future 2032, which addresses the top 10 community issues based on feedback received through the Quality of Life and Asset Management Survey in March 2020, Community Satisfaction Survey in April 2021 and the Community Strategic Plan Survey in October 2021. Consideration was also given to community consultation completed during the development of numerous strategies between 2020 and 2022.

Fourteen priority initiatives were selected for inclusion in the SRV application (through the updated LTFP). They deliver on a cross-section of outcomes from 17 of Council’s strategic documents and can be summarised (with relevant allocations) as follows:

· Sustainable and resilient community – $6,035,096

· Planning for our future – $1,000,000

· Upgrading your community infrastructure – $30,807,000

· Connected walking and cycling paths – $17,982,370

· Protecting bushland and improving open space – $10,283,419

· Improving our technology – $1,150,000

The initiatives include projects associated with community climate change mitigation and adaptation; public amenities; enhanced cyber security maturity; track and trail asset management; track and trail upgrade including accessibility and signage; shared and cycle paths; inclusive community centre; drainage improvement works; Pennant Hills Town Centre review; bushfire risk mitigation; bushland reserve asset management; park amenities renewal and upgrade; new and upgraded play spaces; and a social inclusion program similar to the Hello Hornsby event program. It is noted that any capital costs associated with these projects are in excess of what can be levied through development contributions.

_______________________________

Public Exhibition Process

As part of its decision at the 28 September 2022 General Meeting to progress down the path of an SRV application for 2023/24, Council endorsed an SRV Community Engagement Action Plan and its supporting documents (an SRV Background Paper and an Assessment of Capacity to Pay Report) to assist in seeking community feedback in relation to Council’s intent to make application to IPART for an SRV in respect of the 2023/24 financial year.

The Community Engagement Action Plan outlined the approach, purpose and goals, development of key messages and the timeline for community consultation on a potential SRV application. The Plan was developed to ensure that it meets the SRV assessment criteria set out by the OLG, who sets policy and oversees the local government industry, and IPART, who will assess any SRV application submitted. It was also developed in compliance with Council’s Community Engagement Policy and Community Engagement Plan, as well as the International Association for Public Participation (IAP2) Australasia Quality Assurance Standard.

The purpose of the community engagement was to ensure that the community was adequately informed and consulted about the impact of the proposed SRV and the impact of not applying for an SRV. The objectives of the community engagement process were to:

· Present the proposed SRV

· Identify the impact of the SRV on the average rates across each rating category

· Exhibit an updated LTFP demonstrating the impact of the proposed SRV on Council’s operating results from 2023/24 for feedback and final endorsement by Council

· Communicate to the community the timeline and process for any potential SRV application

· Gather and consider the community’s feedback to inform Council’s final decision on whether and how to move forward with an SRV application.

Council was aware that to meet the assessment criteria for an SRV application, it had to:

· Demonstrate that the need and purpose of a different rate path for Council’s General Fund is clearly articulated and identified in Council’s IP&R documents

· Show evidence that the community is aware of the need for and the extent of a rate rise

· Show that the impact on affected ratepayers is reasonable

· Exhibit, approve and adopt the relevant IP&R documents

· Explain and quantify the productivity improvements and cost containment strategies in its IP&R documents and/or application

· Address any other matter that IPART considers relevant.

While the LTFP for 2022/23 – 2031/32 adopted in July 2022 identified the need for an SRV, it did not model any SRV options. To meet the above criteria, the updated LTFP for 2023/24 – 2032/33, which includes the SRV options, needed to be exhibited, approved and adopted by Council in parallel to the community engagement process.

The Community Engagement Action Plan (and its supporting documents) were drafted in a way to guide communications and community engagement opportunities that provide the public with balanced and objective information to assist them in understanding the problem, alternatives, and preferred solution and to obtain the public’s feedback on analysis and alternatives. Council’s intent was to keep the public informed, listen to and acknowledge concerns and aspirations, and provide feedback on how public input influences the decision to be made by Council.

The timeline outlined in the Community Engagement Action Plan for the progression of the SRV application was in line with the following:

· 4 October 2022 – Commencement of SRV community engagement activities (including the “Have Your Say” project page, emails/newsletters, direct mail, public meetings, social media, advertising, survey, etc) and the commencement of the public exhibition of the draft 2023/24 – 2032/33 LTFP

· 10 October 2022 – Business Ratepayers Forum

· 17 October 2022 – Community Ratepayers Forum

· 25 October 2022 – All Ratepayers and Residents Forum

· 31 October 2022 – All Ratepayers and Residents Forum

· 4 October to 6 November 2022 – Community group presentations (to eight separate stakeholder groups)

· 8 November 2022 – End of SRV community engagement activities and close of public exhibition period for the draft 2023/24 – 2032/33 LTFP

· 23 November 2022 – Council Meeting to consider community feedback in respect of the proposed SRV application; to adopt a 2023/24 – 2032/33 LTFP; and to decide on the progression of an SRV application

· 25 November 2022 – Subject to Council’s decision on 23 November 2022, Council to indicate to IPART its intention to make a SRV application in respect of the 2023/24 financial year.

____________________________________

Council is now in receipt of the Community Engagement Outcomes Report prepared by Morrison Low (copy attached) which details the extensive engagement process undertaken by Council, and Morrison Low (on behalf of Council), between 4 October and 8 November in respect of the exhibition of the LTFP for 2023/24 – 2032/33 and the SRV application proposal.

The Outcomes Report also provides the following summary of the issues that have been raised through submissions:

· The SRV increase is too high and the timing is difficult having regard to cost of living pressures, inflation, interest rates, economic conditions, energy bills, rent rises and mortgages

· Council should increase efficiencies, increase productivity or savings, reduce wastage, reduce overhead costs

· The SRV will have a harder impact on retirees, pensioners, the elderly

· There is an understanding and awareness that Council is facing rising prices

· Development growth in the Shire should be providing enough income for Council

· Council should prioritise essential projects (not wish list) or defer non-essential projects

· Council should tighten its belt – live within its means – or just focus on Council’s essential services

· Council should undertake better financial management

· Council is out of step with the community

· There is dissatisfaction with current levels of maintenance, services, facilities, planning, traffic, overdevelopment, congestion (waste, roads, pathways, parks, trees, stormwater, public amenities, etc)

· The SRV rate increase should not be above the CPI, inflation, wage growth or the IPART rate.

From the commencement of the public exhibition process on 4 October 2022, Council had in place on its website a Q&A page which covered the issues it was expecting to be raised by members of the public about the SRV application proposal. That Q&A page has been updated during the exhibition process to reflect further matters raised online and through submissions by members of the public. A selection of the Q&As (which respond to most of the issues identified by the community as summarised above) together with additional information and responses is provided below.

How will the proposed special rate variation impact my rates?

While we understand that everyone is under pressure with rising costs, we too are navigating these same issues and we have a duty of care to manage Council’s budget responsibly. Rates would rise by 8.5% in 2023/24, 7.5% in 2024/25, 6.5% in 2025/26 and 5.5% in 2026/27, which represents an increase of 31.05% (cumulative) staged over four years, including the annual rate peg set by IPART.

For residents currently paying our average rate, this would mean an increase of $2.07 a week in the first year. For business ratepayers, the weekly increase on the average rate would be $3.97 in the first year. Rates are levied on properties in accordance with their categorisation; residential, business or farmland. Council also has two special business sub-categories: Hornsby CBD and Major Retail Shopping Centre. The impact on average rates in each category is provided in the table below.

|

Rating category |

2022-23 |

2023-24 |

2024-25 |

2025-26 |

2026/27 |

Cumulative increase |

|

Residential |

$1,272.79 |

$1,380.98 |

$1,484.55 |

$1,581.05 |

$1,668.01 |

$395.21 |

|

Business |

$2,437.00 |

$2,644.15 |

$2,842.46 |

$3,027.22 |

$3,193.71 |

$756.71 |

|

Farmland |

$2,133.64 |

$2,315.00 |

$2,488.63 |

$2,650.39 |

$2,796.16 |

$622.52 |

|

Major Retail Shopping Centre |

$268,650.80 |

$291,486.12 |

$313,347.58 |

$333,715.17 |

$352,069.50 |

$83,418.70 |

|

Hornsby CBD |

$5,149.14 |

$5,586.82 |

$6,005.83 |

$6,396.21 |

$6,748.00 |

$1,598.86 |

What is the alternative to the proposed rates increase?

Council must apply sound financial principles in managing its resources under the Local Government Act. This includes ensuring that revenues and costs align. The alternative to the proposed rate increase would be a significant reduction in spending on services and assets to ensure that Council does not spend more than it earns.

Council has forecasted in the LTFP that to deliver the current services and sufficiently maintain assets over the next 10 years, it would incur increasing operating deficits. Council would need to cut spending on services and assets by approximately $3.6 million per year over the 10 years to ensure that forecasted costs align with forecasted revenues, noting that the deficit that will be required to be funded or otherwise eliminated in 2033 is above $8 million.

Whilst decisions regarding service reductions and further efficiencies will in themselves be subject to consultation over the upcoming period to the adoption of a revised LTFP and Budget for 2023/24, some of the specific options to be considered include the following:

o Closing the outdoor 50 metre pool at the Aquatic Centre during the cooler months and/or reviewing charges for use of the facility, noting that Council’s costs to heat the pool are increasing significantly.

o Reducing library hours to core business hours; closing lesser utilised branch libraries; and closing or reducing public access to the Community Recycling Centre.

o Reducing levels of park and sportsfield maintenance through the employment of less staff and contractors; and downgrading of the community nursery.

o Reducing resources to respond to community requests for service in areas such as environmental compliance, noise, nuisance flooding, cleansing of public areas such as toilets, community events, bushland and other natural resource management, place management activities, street sweeping, and tree inspections (both public and private trees).

While every effort will be made to ensure that the impacts on services the community utilise are minimised and Council will seek to reduce resources (costs) where the impact will be least felt, it must be recognised that there will be an increase in community dissatisfaction with Council and with the quality of life enjoyed by the Hornsby Shire community.

Our current financial forecasts also indicate that without an SRV, we would have insufficient capacity to fund the recurrent cost of operating major new capital projects once construction is complete. This includes Hornsby Park and Westleigh Park, noting the construction of these projects is funded from external sources. Without the SRV, we also would not have the capacity to fund the key strategic initiatives that our residents have told us are important to them, as outlined on the main project page.

What action has Council taken to address its financial situation and minimise rate increases?

Over the last 10 years, Council has implemented a range of cost containment strategies which have resulted in Council delivering an average of $6.2 million in annual ongoing costs savings and revenue improvements, with a further $3.2 million in one-off costs savings and revenue improvements. These figures were independently verified by an external financial consultant. Since 2012, this has delivered a total of $52.5 million in benefits that were reinvested in service delivery and infrastructure. These savings are a result of:

o Savings found and implemented from a review of internal services in 2012.

o Savings found and implemented from a review of external services in 2013.

o Vigilant budgetary management through the quarterly review process, identifying and ring-fencing savings throughout the financial year.

o Utilising savings achieved to reduce the need for debt to fund the Hornsby Aquatic and Leisure Centre in redevelopment from 2013, resulting in an annual average interest savings of $513,000 thousand over the 20-year life of the loan.

In addition to these savings, Council implemented a general freeze on any increase to non-labour operational expenditure, unless grants and/or fees and charges could support an increase, in 2014/15 and again in 2017/18. In 2014/15, this resulted in costs being contained to a 1.1% increase. Our LTFP Plan also recommends a range of actions, in addition to the SRV, to improve the financial direction including:

o Review other income streams such as fees and charges to ensure appropriate price setting and assess whether price increases could be used to generate additional income.

o Continuation of current freeze to Council’s approved Full Time Equivalent headcount; with no new positions to be created unless offset by an equivalent position elsewhere.

o Maintain cost increases to modest levels in regard to non-labour related expenses each year, excluding the additional allowances that have been made in the LTFP including annual allocations for asset management and strategic initiatives.

o No new loan borrowing to be undertaken unless financial capacity above a 2% budget surplus/operating performance ratio is available each year in the Plan.

o Continuance of financial improvement initiatives (the development of business improvement plans and the conduct of service reviews).

o Consider whether there is a case to rationalise underutilised assets to reduce ongoing cost requirements and/or provide one off capital funding from sale proceeds towards other capital investment decisions.

Given Council’s ongoing and one-off savings that have been found and implemented over an extended period, it is not expected that the quantum of further savings (and revenue growth from fee increases or new income streams) will in themselves resolve the financial challenges that Council is facing

Can’t you get more funding from other levels of government to help pay for things?

Where possible, Council applies for grants for specific projects and initiatives. However, these grants can only be applied to the initiatives for which they were provided for and not ‘business as usual’ activity like asset maintenance. Further, it cannot be assumed that Council will be successful in being awarded a grant, therefore this makes future planning difficult to predict.

Council’s share of revenue from the Commonwealth and State Governments has in real terms fallen substantially over the last decade. In fact, cost shifting from other levels of government is exacerbating our income cost balance

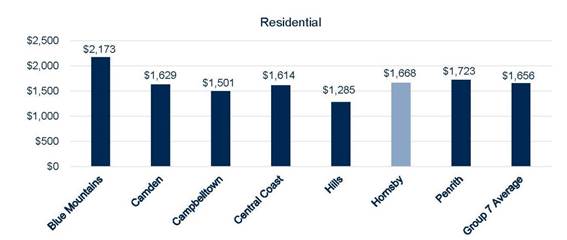

How does Hornsby Shire Council compare to other councils in terms of how much rates we pay? And what will it look like following the SRV?

The Office of Local Government groups councils with other similar councils for comparison. Hornsby Shire Council is in Group 7 with other metropolitan fringe councils such as Blue Mountains, Camden, Campbelltown, Central Coast, The Hills and Penrith councils. In comparison to these councils, Hornsby Shire Council’s rates are relatively competitive.

|

Category 7 – Council Name |

Average Residential Rate 2022/23 |

|

Blue Mountains |

$1,917.62 |

|

Camden City Council |

$1,396.00 |

|

Campbelltown City Council |

$1,319.80 |

|

Central Coast |

$1,423.00 |

|

Hills Shire Council |

$1,129.43 |

|

Hornsby |

$1,272.79 |

|

Penrith |

$1,520.82 |

|

Overall Average |

$1,425.64 |

Our rates are also competitive in comparison with the other councils in the Northern Sydney Regional Organisation of Councils (NSROC).

|

NSROC Council Name |

Average Residential Rate 2022/23 |

|

Hornsby |

$1,272.79 |

|

Hunters Hill |

$1,989.90 |

|

Ku-ring-gai |

$1,577.65 |

|

Lane Cove |

$1,286.00 |

|

Mosman |

$1,558.00 |

|

North Sydney |

$838.21 |

|

Ryde |

$1,066.12 |

|

Willoughby |

$1,048.19 |

|

Overall Average |

$1,329.61 |